Infocorp is a Uruguayan company that implements omnichannel platforms for digital banking, among other services. It was recently acquired by Constellation Software Inc. (CSI), a Canadian group, with which it seeks to expand to the United States, Canada and Europe. Infocorp currently has more than 50 Latin American banks in its client portfolio. Ana Inés Echavarren, CEO of Infocorp, gave an interview to El Periódico about its arrival in the Guatemalan market.

Infocorp is a Uruguayan company, but how did it start its expansion process?

– We have been in the market for 25 years and the Uruguayan market, being so small, generally requires service companies to start thinking about exporting. In Uruguay, we started making digital channels for the country’s Santander bank, which in fact was one of the first to implement home banking in Latin America. Infocorp’s expansion started with referrals, and we began an expansion in Latin America almost unintentionally.

Currently, the firm is immersed in a process of regional expansion and Guatemala is one of the markets Infocorp is aiming at.

– Guatemala was one of the countries in the region with which we had not worked and last year, Banco G&T Continental honored us by selecting Infocorp to implement its new digital channels platform. In the midst of the pandemic, we just came out with the first phase of its digital transformation, which was an application for companies. We are very happy with the job and to start working in Guatemala.

What business opportunity do you see in the country?

– There are a lot of opportunities in the market. Although financial services may be lacking a bit of technology, Guatemala is a country that is making progress. For example, many times, being able to open accounts one hundred percent digitally from a cell phone has to do not only with technology but with security measures regulation, superintendencies and with the most banked sector of the population, among others.

Have you had contact with more local banks?

– It is confidential information, but we have had contact with several banks. The country is a market where there is a desire to do things, and as in all of Latin America, there is still a long way to go. If one can see something positive about this COVID-19 crisis, it is that it has accelerated digital adoption. Guatemala is no stranger to this reality, in fact, it is one of the countries where banks did not stop operating and the financial market has responded well, thanks to the fact that the sector was already going through digital transformation projects.

Accelerating digitization in the financial sector is one of Infocorp’s objectives. What solutions do you offer?

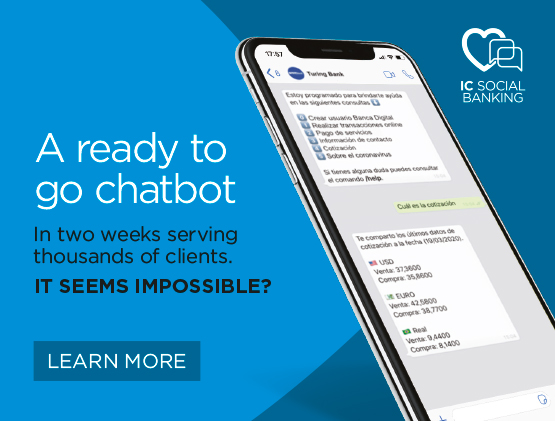

– Today, having a platform for digital channels is essential. Users need to be able to pay for services, transfer money, check their accounts or pay someone digitally. It is not only the platform but also the digital channels. In these last months, WhatsApp has been the preferred digital channel. This was the largest number of deployments for us. In the midst of the pandemic, we confirm the priority of chatbots. We were already investing and evolving in this product.

Do you work on innovations?

– Today we are considering the possibility of enabling banks to carry out transactions with each other and letting client companies use banks as platforms to make transactions. That is called “Open Bank”, and it is a trend that was already very strong. We are working on that today, in a pilot phase with some clients. And the other thing is retail banking. There is a very large percentage of bank customers who only use cell phones as a means of communication, so it is necessary to have an intelligent native application that adapts to each user. We are working on this, for me, not only it is the channel of your choice, but also a 100% personalized experience.

What challenges is Infocorp facing during the implementation of this technology in the sector?

– To some extent, the crisis helped to break down resistance to change. Typically, 20 to 30 percent of people were making their bank transactions online. We don’t have our customer data yet, but I’d say we went from 20 percent to 50 or 60 percent in a matter of weeks. Then we have the banking regulations. It is difficult to choose between wanting to make the user’s life easier and guaranteeing secure transactions. In recent months, several barriers have been broken down, but it is still difficult to have a 100 percent digital procedure.